Note

Click here to download the full example code

Discount factor convergence#

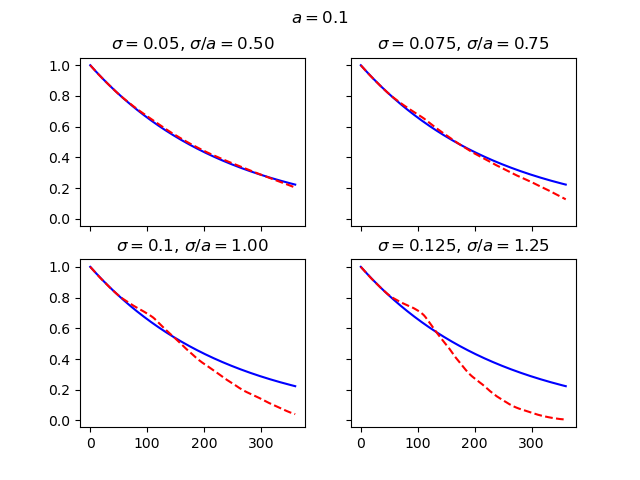

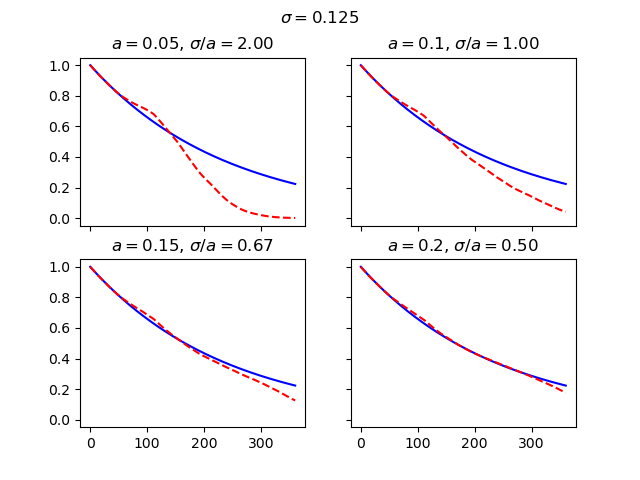

The convergence of the stochastic discount factors generated by the Hull-White model.

The charts below examine the convergence of the discount factors for various combinations of \(\sigma\) and \(a\), first by changing \(\sigma\) and secondly by changing \(a\). As Balaraman’s study shows, the convergence gets worse as \(\sigma/a\) gets larger than 1, and gets better as \(\sigma/a\) gets smaller than 1.

See also

Overview of BasicHullWhite notebook in the

economiclibrary

import modelx as mx

import matplotlib.pyplot as plt

HW = mx.read_model("BasicHullWhite").HullWhite

fig, axs = plt.subplots(2, 2, sharex=True, sharey=True)

fig.suptitle(r"$a=$" + str(HW.a))

for sigma, (h, v) in zip([0.05, 0.075, 0.1, 0.125], [(0, 0), (0, 1), (1, 0), (1, 1)]):

HW.sigma = sigma

axs[h, v].set_title(r"$\sigma=$" + str(sigma) + r", $\sigma/a=$" + "%.2f" % (sigma/HW.a))

axs[h, v].plot(range(HW.step_size+1), [HW.mkt_zcb(i) for i in range(HW.step_size+1)], "b-")

axs[h, v].plot(range(HW.step_size+1), HW.mean_disc_factor(), "r--")

fig, axs = plt.subplots(2, 2, sharex=True, sharey=True)

fig.suptitle(r"$\sigma=$" + str(HW.sigma))

HW.sigma = 0.1

for a, (h, v) in zip([0.05, 0.1, 0.15, 0.2], [(0, 0), (0, 1), (1, 0), (1, 1)]):

HW.a = a

axs[h, v].set_title(r"$a=$" + str(a) + r", $\sigma/a=$" + "%.2f" % (HW.sigma/HW.a))

axs[h, v].plot(range(HW.step_size+1), [HW.mkt_zcb(i) for i in range(HW.step_size+1)], "b-")

axs[h, v].plot(range(HW.step_size+1), HW.mean_disc_factor(), "r--")

Total running time of the script: ( 0 minutes 1.617 seconds)